AbaWeb

AbaWeb

Säule 3a

Die Berufliche Vorsorge (2. Säule) ist seit Jahren unter Druck. Als Faktoren zu nennen sind hier z.B. die demographische Entwicklung, die steigende Lebenserwartung, die laufenden (zu hohen) Rentenleistungen, das Tiefzinsumfeld im Finanzmarkt sowie die gesetzlichen Anlagebeschränkungen. Aufgrund dieser Faktoren ist die Verzinsung der angesparten Vorsorgeguthaben in der 2. Säule in den letzten Jahren kontinuierlich gesunken und auch die Rentenumwandlungssätze werden laufend nach unten korrigiert. Nicht zu vergessen die hohe Querfinanzierung der laufenden Rentenleistung durch die heutigen Beitragszahler. Und trotzdem – die 2. Säule bleibt einer der wichtigsten Pfeiler in der Altersvorsorge. Die gebundene freie Vorsorge (Säule 3a) gewinnt dabei aufgrund der vorgenannten Problematik in der 2. Säule immer mehr an Bedeutung.

Die Säule 3a ist die individuelle Altersvorsorge und wird durch die steuerliche Privilegierung von Bund, Kantonen und Gemeinden gefördert. Mit einer Einzahlung in die Säule 3a kann die Altersvorsorge verbessert und die Steuerbelastung gesenkt werden. Jeder einbezahlte Franken kann vom steuerbaren Einkommen abgezogen werden. Der jährliche Beitrag ist für Selbständigerwerbende und Angestellte mit einem Pensionskassenanschluss auf CHF 6'883 (ab 2021) beschränkt. Erwerbstätige ohne Pensionskassenanschluss können jährlich bis zu 20% des Erwerbseinkommen, jedoch höchstens CHF 34'416 (ab 2021) einzahlen. Beiträge dürfen bei Erwerbstätigkeit bis max. fünf Jahre nach Erreichen des ordentlichen Rentenalters geleistet werden.

Die 3a Guthaben können frühestens fünf Jahre vor Alter 64 bei Frauen und Alter 65 bei Männern bezogen werden. Wird die Erwerbstätigkeit länger fortgeführt (über das ordentliche Pensionsalter hinaus), müssen die Altersguthaben spätestens bis Alter 69 für Frauen bzw. Alter 70 für Männer bezogen werden. Unter gewissen Umständen ist ein vorzeitiger Bezug vor dem 59. oder 60. Altersjahr möglich. Zum Beispiel bei Erwerb oder Sanierung von selbstbewohntem Wohneigentum, bei der Aufnahme einer selbständigen Erwerbstätigkeit oder bei einer Auswanderung (Aufzählung nicht abschliessend).

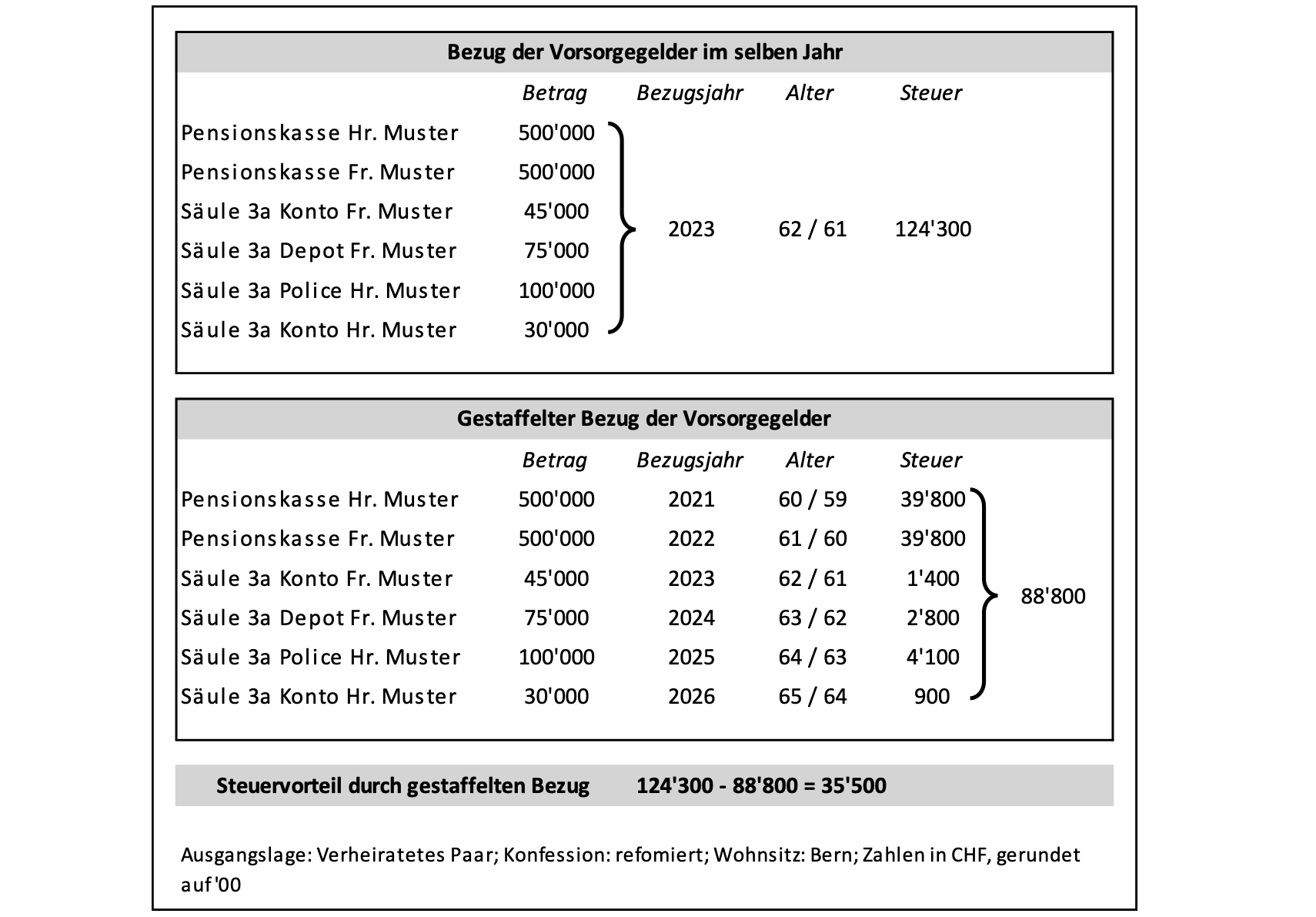

Beim Bezug der 3a Guthaben unterliegt das Kapital einer Kapitalauszahlungssteuer (analog 2. Säule). Die Höhe der Kapitalauszahlungssteuer hängt von der Höhe des ausbezahlten Betrages ab. Aufgrund des progressiven Steuersatzes gilt: Umso grösser der Betrag, desto grösser die Steuerbelastung. Deshalb sollte der Bezug der Vorsorgegelder gestaffelt auf verschiedene Steuerperioden geplant werden. Dabei gilt es, den Bezug der 3a Guthaben (Konto, Wertschriftendepot, Versicherungspolice) mit dem Bezug aus der 2. Säule (Pensionskasse, Freizügigkeitsguthaben) zu koordinieren (siehe nachfolgende Tabelle).

Da die bezogenen 3a Guthaben nach dem Bezug dem steuerbaren Vermögen zugerechnet werden, lohnt es sich, den Bezug möglichst lange hinauszuzögern. So können Vermögenssteuern gespart werden. Es gilt hier aber auch die Steuervorteile bei einem gestaffelten Bezug im Auge zu behalten.

Bei fehlender Liquidität für die Optimierung in der Beruflichen Vorsorge (kurz vor der Pensionierung) kann es durchaus auch sinnvoll sein, seine 3a Guthaben zu beziehen und in die Berufliche Vorsorge einzuzahlen. Wichtig ist, dass das Kapital zuerst auf ein privates Konto transferiert wird, bevor es anschliessend in die Pensionskasse fliesst. Dabei werden zwar Kapitalauszahlungssteuern auf den bezogenen Guthaben fällig, der in die Berufliche Vorsorge eingebrachte Betrag kann aber vom steuerbaren Einkommen abgezogen werden. Es findet kein steuerpflichtiger Vermögenszuwachs statt. Sparturbo, da mit einem reduziert besteuerten Bezug ein voller Steuerabzug generiert wird!

Die Optimierungsmöglichkeit «Bezug Vorsorgeguthaben 3a mit unmittelbarem Einkauf in die Berufliche Vorsorge» ist im kürzlich publizierten Bundesgerichtsentscheid vom 14. Mai 2020 bestätigt worden. Falls bei der Pensionierung ein Kapitalbezug aus der Pensionskasse geplant ist, gilt es zu beachten, dass der letzte Einkauf zwingend 3 Jahre vor dem Kapitalbezug stattfindet.

Berufliche Vorsorge, gebundene Vorsorge 3a und Steuern; eine komplexe Materie mit vielen Fragen und Antworten, bei welchen wir Ihnen im Rahmen einer Vorsorgeberatung gerne unterstützend zur Seite stehen.

Valentin Chiquet

Finanzplanung & Vorsorgeberatung

BSc HES-SO in Betriebsökonomie

vch@core-partner.ch